.

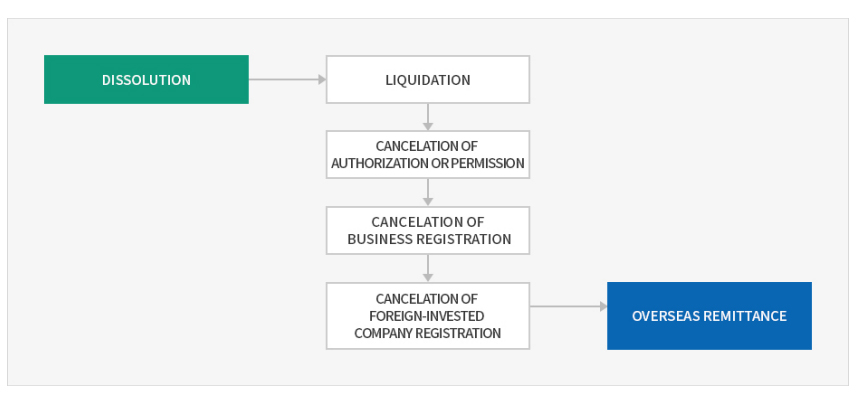

When a corporation discontinues its business, its corporate personality is lost through a procedure of dissolution, liquidation, cancelation of authorization or

permission, cancelation of business registration, and cancelation of the foreign-invested company registration, all of which takes about two months. It is

impossible to shorten the period to less than two months since the period of notice to creditors must not exceed two months in accordance with Article 535 of

the Commercial Act.

The process of dissolution and liquidation is required for the elimination of corporate personality. The grounds for dissolution are as follows, but in most cases, the dissolution is decided by a resolution passed at a general meeting of shareholders.

Grounds for Corporate Dissolution

Termination of the period of existence or occurrence of any events specified in the articles of incorporation

Merger

Bankruptcy

Order or judgment of a court

Division or merger after division of the company

Resolution passed at a general meeting of shareholders (by more than two-thirds of shareholders present and more than one-thirds of the total issued shares

Appointment of Liquidators

Upon dissolution of a company, except in cases of dissolution by a merger, division, merger after division, or bankruptcy, directors shall become liquidators.

This shall not be applied if otherwise provided for in the articles of incorporation or if other persons have been appointed at a general meeting of shareholders.

Reports of Liquidators

A liquidator must report the grounds for and date of dissolution and the name, resident registration number and address of the liquidator to the court within two weeks of the date of appointment.

Investigation and Report of Company Assets

After a liquidator has assumed office, that person must, without delay, investigate the status of the company’s assets, prepare an inventory list and a balance

sheet, and submit them to a general meeting of shareholders for approval.

Preparation and Submission of Balance Sheets, etc.

A liquidator must prepare a balance sheet, supplementary schedules, and a business report four weeks prior to the date set for an ordinary general meeting of shareholders, and submit them to an auditor.

Submission of Audit Reports from Auditors

An auditor will submit an audit report on the balance sheet, supplementary schedules, and a business report to a liquidator one week prior to the date set for an ordinary general meeting of shareholders.

Peremptory Notice to Creditors and Repayments

Liquidators must give peremptory notices to company creditors, by means of public notice, at least two times within two months after taking office, to the effect that creditors may present their claims within a fixed date and that any creditor failing to do so will be excluded from the liquidation. In addition, liquidators must give peremptory notices demanding presentation of claims individually to each creditor known to the company in question, and such creditors must not be excluded from the liquidation, even if they have failed to present their claims.

Distribution of Surplus Assets

Surplus assets are to be distributed to shareholders in proportion to the number of shares held by each shareholder.

Completion of Liquidation

When liquidation-related affairs have been completed, a liquidator shall, without delay, prepare a statement of the settlement of accounts and submit it to a

general meeting of shareholders for approval.

Registration of the Completion of Liquidation

After the completion of liquidation, liquidators shall register the completion of liquidation upon the approval of a general meeting of shareholders within two

weeks for main branches, or within three weeks for other branches.

Cancellation of Authorization, Permission, or Business Registration

Cancelation of Authorization or Permission

Where registration of business, report of business, and authorization or permission of business are granted by the type of established business, business closure must be reported. The managing authority is a borough office of si/gun/gu/special self-governing province, a local community health center in jurisdiction, or a local ministry of food and drug safety where the authorization or permission was initially issued.

Cancelation of Business Registration

When a business operator closes registered business, the operator must submit a declaration of business closure, without delay, to the head of the tax office

(submission acceptable through the national tax information network).

Cancelation of a Foreign-Invested Company Registration

When a foreign-invested company closes its business, foreign-invested company registration must be canceled. The delegated agency will issue a confirmation of cancelation of the foreign-invested company registration after the completion of cancelation.

Overseas Remittance

Collection of surplus equity for investment and overseas remittance are guaranteed by Article 3.1 of the Foreign Investment Promotion Act and Article 6.1 of the Foreign Exchange Transactions Act.

Whatsapp : +82 10-6271-9185 / FAX : +82 2-2631-2230 /

Whatsapp : +82 10-6271-9185 / FAX : +82 2-2631-2230 /